Ancient Romans compared wasted effort to plowing the seashore.

In a capitalist economy, one is hard-pressed to find examples where such activity can persist for very long. One glaring exception is active funds management. Despite decades of under performance, this industry still thrives, managing trillions in assets and generating an estimated $224 billion in fees globally in 2024.

Active management persists in its current form for a mix of reasons but the writing is on the wall. AI is poised to profoundly transform this industry. While some roles face significant disruption, the industry's core value - generating alpha through nuanced, context-aware strategies - will likely remain human-dependent for the foreseeable future. However, fee compression and shifting talent will favor more AI-savvy firms.

Active management persists in its current form for a mix of reasons but the writing is on the wall. AI is poised to profoundly transform this industry.

This particular missive takes aim at an industry that has been in denial for years. We will present some incontrovertible evidence, in the form of S&P Global’s SPIVA Scorecards, to set aside any doubt about active funds’ underperformance. It is a clarion call, to shake the industry out of its torpor and to embrace a technology that offers promise: artificial intelligence.

Active fund (under)performance

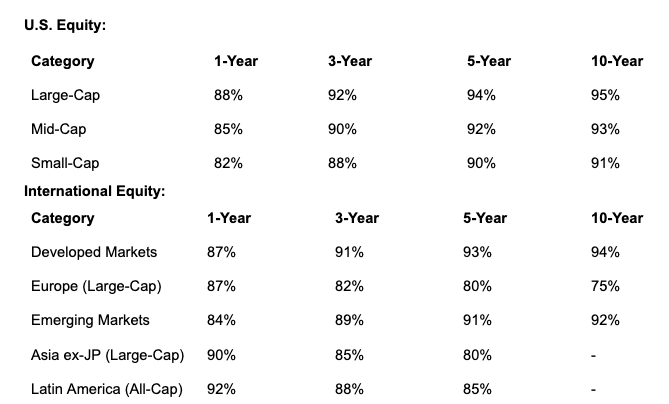

Each quarter, S&P Global produces reports that compare the performance of actively managed funds against their passive benchmarks. For example, they compare the performance of active US large-cap funds against the S&P 500.

These reports, known as the SPIVA (S&P Indices Versus Active) Scorecards, consistently demonstrate that the majority of active fund managers underperform their benchmarks over most time horizons. For instance, over 15 years, more than 90% of U.S. large-cap active equity funds lag the S&P 500.

The 2025 Mid-Year Scorecard (as of June 30, 2025) covers US and international equity/fixed income funds. The principal findings are shown in Figures I and II.

The more efficient the market, the worse we expect active managers to perform. The US equity results suggest that the US market is highly efficient with less than 10 percent of US equity fund managers outperforming over five years across all market capitalization categories.

The results for international equity funds are equally poor, even though we typically expect emerging markets to be less efficient. Not surprisingly, given these performance statistics, many funds do not survive. The S&P data shows that around 40% of US equity funds disappear within 10 years. The number for international funds is slightly higher, at around 45%.

Regional results vary. Over a five-year horizon, the underperformance percentage ranges from 91.4% in the efficient European markets to 58.1% in the relatively inefficient markets of Middle East and North Africa. But the principal message remains the same: The vast bulk of active managers underperform.

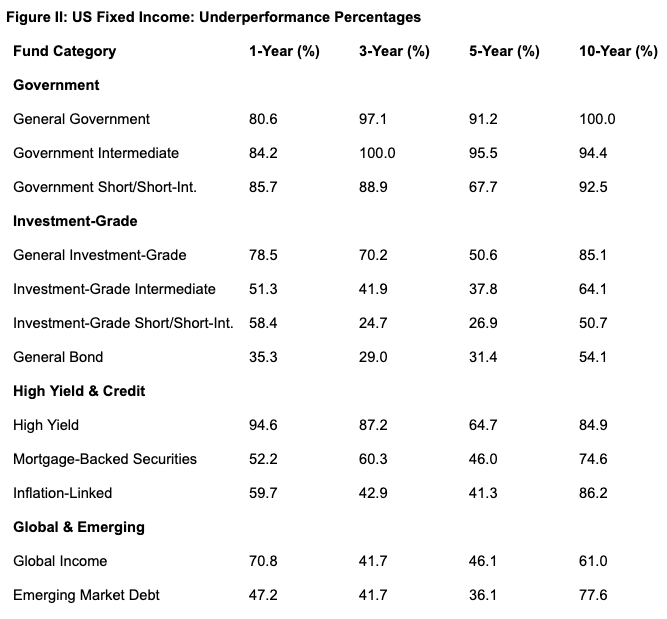

The performance of active fixed-income funds is more nuanced, with active investors performing better in shorter-term bonds and in markets with wider differences in yields, such as emerging markets. As with equities, the underperformance of active fixed income tends to worsen over time, suggesting that active funds that do outperform have difficulty sustaining superior returns. This explains why the survivorship rates of fixed income largely mirror those of active equity.

Active funds’ inability to outperform in high yield is noteworthy. It suggests that investors are poor at anticipating corporate failure. This is an area, incidentally, where Transparently.ai achieves 90% accuracy and thus could be of great benefit to high-yield portfolio selection.

Implications

The implications of the SPIVA results are stark. If the participants in any other industry were confronted by this kind of performance data, serious restructuring efforts would be under way.

The data bolsters the global argument for low-cost passive strategies. Naturally, active funds' higher fees (often 0.5-1.0% vs. <0.1% for ETFs) exacerbate the underperformance. While active strategies may shine in niche or volatile periods, the odds favor broad-market index funds for most investors.

Fund flows reflect the data. In 2024, active strategies faced $0.1 trillion in net outflows, primarily driven by outflows from active equity mutual funds. Within this total, active fixed-income funds saw strong inflows of ~$700 billion globally, and active ETFs attracted $325 billion (mostly from North America). Passive funds, by contrast, saw $1.7 trillion in inflows. Equity index funds drove much of this inflow.

Given the consistent underperformance, and the direction of fund flows, the question arises: what is the path forward?

The future

Unless active investors, particularly in equity and credit, find a way to re-invent themselves, the trend towards diminishing market share and shrinking fees appears destined to persist.

Fortunately, a promising solution is emerging in the form of AI.

The CFA Institute's Enterprising Investor blog (March 13, 2024) provides strong evidence through its analysis of Engineered Alpha Management (EAM), an AI-powered active management approach. It reports that EAM portfolios delivered an average annual excess return of 516 basis points over benchmarks across all nine US equity style boxes, with nine out of nine lead funds outperforming—a level of consistency unmatched by other active fund families.

Success rates for outperformance were measured over rolling one-, three-, and five-year periods, highlighting AI's role in generating statistically significant, persistent alpha via data-driven portfolio construction. This suggests AI can help managers beat benchmarks more reliably by leveraging vast datasets.

More recently, a McKinsey & Company report (July 16, 2025) supports this indirectly, noting that generative AI tools enable portfolio managers to "refine strategies, narrow investment options, and optimize portfolio construction," with an 8% efficiency impact in investment management. That potentially translates into more consistent outperformance through faster, data-enriched decisions.

To be sure, the work undertaken by the data scientists here at Transparently also provides compelling evidence that the incorporation of our AI-driven risk metrics can greatly enhance portfolio returns.

As more active managers begin to incorporate AI tools into their investment processes, we anticipate the performance of active managers will begin to improve relative to passive. Certainly we would expect to see a big improvement by 2030.

That said, a lot of active managers will be left in the cold. Based on our interaction, many remain deeply skeptical of AI approaches and appear reluctant to incorporate AI into their core investment processes. These managers will eventually discover they have brought a knife to a gun fight.