As economic conditions become increasingly uncertain - driven by rising interest rates, global supply chain pressures, and the re-escalation of U.S. tariffs - investors face a growing disconnect between equity valuations and underlying fundamentals.

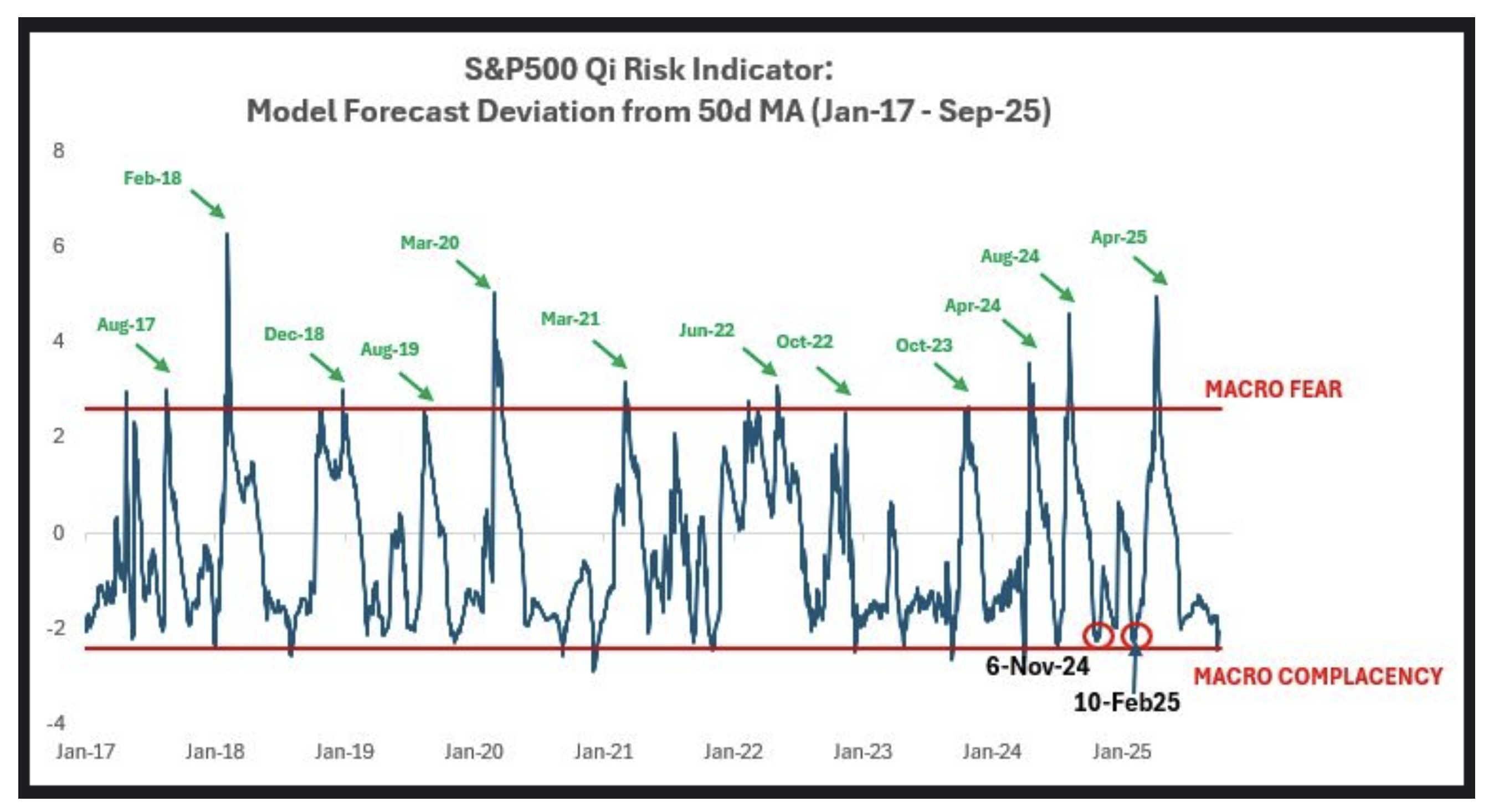

Stock markets continue to trade at elevated forward earnings multiples, even as corporate profit margins come under pressure from higher input costs, weakening consumer demand, and geopolitical instability. Macro risk models show we’re at peak complacency and asset allocators are actively looking for experienced tail risk funds to invest in.

This disconnect raises an important question: Are companies adjusting to this economic transition honestly, or are we entering a phase where financial reporting becomes less reliable?

At Transparently, we believe we’re approaching a critical inflection point. Our models suggest that rising economic stress and valuation pressure could incentivize companies to smooth earnings, obscure margin erosion, or even commit outright financial misreporting. As part of our risk analytics platform, we've built tools to detect the early warning signs of accounting manipulation, before it becomes visible in headline numbers or results in costly investor losses.

Coming pressure on reported earnings

The latest round of U.S. tariffs will feed through to company cost structures in the months ahead, particularly in manufacturing and consumer sectors. As margins tighten, companies face a choice: revise guidance downward and risk market backlash, or find ways to sustain headline earnings.In some cases, this leads to “earnings smoothing” within accounting norms.

In others, it can cross the line into manipulation or worse, fraud. The challenge for investors is that these practices are rarely obvious in real time. Financial statements are complex, and irregularities are often masked by timing differences, accounting estimates, or balance-sheet adjustments.

Earnings pressure and incentives to manipulate

Research has consistently shown that financial reporting quality is pro-cyclical. It deteriorates in boom times when incentives to sustain high valuations are greatest and often unravels in downturns when poor performance is harder to hide.

Several key academic studies support this view:

- Burns & Kedia (2006) found that companies with option-heavy CEO compensation were more likely to engage in aggressive accounting during the 1990s bull market, driven by pressure to meet high valuations.

- Cohen, Dey & Lys (2008) observed that a wave of corporate scandals (e.g., Enron, WorldCom) emerged at the tail end of an economic expansion, right before Sarbanes-Oxley regulation. The boom conditions created space for manipulation; the subsequent downturn revealed it.

- Povel, Singh & Winton (2007) reinforced this point through a dynamic model of corporate fraud: manipulation is more likely in good times but more likely to be uncovered in bad times. Strong growth hides weak fundamentals; recessions expose them.

- Richardson, Tuna & Wysocki (2010) analyzed the 2008 financial crisis and found that banks and financial institutions had overstated assets and understated risks through opaque instruments and valuation assumptions - tactics that unraveled quickly as the downturn set in.

Today’s market: A set-up for dislocation

We see similar conditions developing today. Corporate earnings guidance remains optimistic, while macroeconomic data points to deceleration. The latest round of tariffs may further compress margins, particularly in manufacturing and consumer sectors. Yet, equity prices remain resilient.

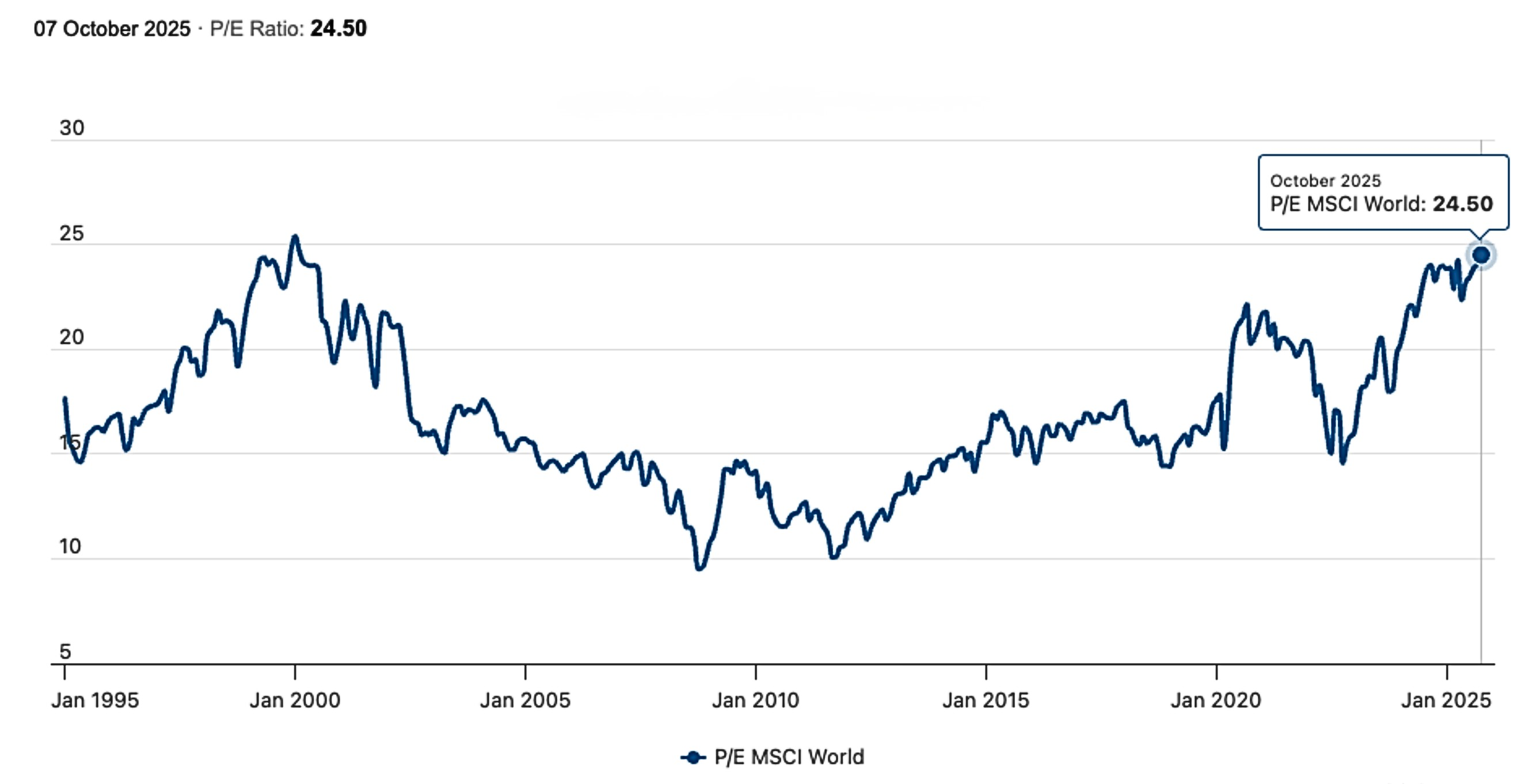

This leads to a bifurcation: either companies will revise down earnings expectations-potentially triggering market corrections-or investors will be asked to accept even higher forward multiples, compounding valuation risk. As the below chart shows, we are already at peak equity multiple on MSCI World.

In such an environment, CFOs under pressure to maintain appearances may resort to short-term earnings management techniques-changes in depreciation schedules, one-off adjustments, or aggressive revenue recognition policies. While some tactics fall within the bounds of GAAP, the line between earnings smoothing and misstatement can blur quickly.

Transparently.ai: Detecting manipulation before it makes headlines

At Transparently, we’ve developed a risk-detection platform that applies forensic accounting and statistical pattern recognition to public financial statements. Our models are designed to identify anomalies and red flags that may indicate manipulation or financial reporting risk-long before restatements or regulatory actions occur.

Our methodology includes:

- Forensic accounting ratios such as modified Beneish M-Scores and accrual quality indicators

- Balance sheet and income statement pattern analysis, detecting unusual trends in revenue recognition, working capital changes, and discretionary accruals

- Cross-sectional peer benchmarking to flag deviations from sector norms

- Machine-learning models trained on historical fraud cases to identify suspicious financial statement behavior

By focusing on the financials - not sentiment or market signals - we offer a disciplined, data-driven approach to identifying companies at higher risk of accounting manipulation or distress. Our goal is not to "catch fraud" in hindsight but to highlight the subset of companies where investors should demand greater scrutiny before a negative surprise occurs.

Why this matters now

In the months ahead, we expect to see earnings surprises, downward revisions, and, in some cases, restatements or enforcement actions. Companies facing deteriorating fundamentals may be tempted to obscure the extent of the impact, especially if market valuations remain high and investor expectations elevated.

For institutional investors, portfolio managers, and regulators, the key challenge is separating companies managing through tough conditions from those masking deeper problems. Forensic analytics, applied systematically and proactively, can help identify those outliers before losses crystallize.

About Transparently.ai

Transparently.ai is a financial risk intelligence platform that uses forensic accounting and advanced pattern recognition to detect signs of accounting manipulation and fraud. Our models analyze financial statement data to provide early warning signals on companies at risk-helping investors, lenders, and regulators make more informed decisions.

Contact us for a demo or to learn more about how our models can support your investment or risk-management process.